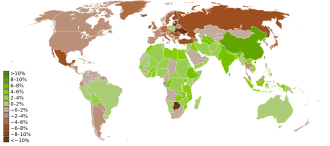

The Great Recession was a period of market decline in economies around the world (particularly in the western world and associated countries) that occurred from late 2007 to mid-2009, overlapping with the closely related 2008 financial crisis. The scale and timing of the recession varied from country to country (see map). At the time, the International Monetary Fund (IMF) concluded that it was the most severe economic and financial meltdown since the Great Depression of the 1930s.

The Great Recession was caused by many weaknesses that slowly developed in the global financial system, along with a series of triggering events that began with the bursting of the United States housing bubble in 2005–2012. When housing prices fell and homeowners began to abandon their mortgages, the value of mortgage-backed securities held by investment banks declined in 2007–2008, causing several banks to collapse or be bailed out in September 2008. This 2007–2008 phase became known as the subprime mortgage crisis.

The combination of banks being unable to provide funds to businesses and homeowners paying-down debt (rather than borrowing and spending) resulted in the Great Recession. In the U.S., the recession officially began in December 2007 and lasted until June 2009, thus extending over 19 months. As with most other recessions, it appears that no known formal theoretical or empirical model succeeded in accurately predicting the onset of this recession, except for minor signals in the sudden rise of forecast probabilities, which were still well under 50%.

The recession was not felt equally around the world; whereas most of the world's developed economies, particularly in North America, South America and Europe, fell into a severe, sustained recession, far less impact occurred in many more-recently developing economies, particularly in China, India and Indonesia, whose economies grew substantially during this period. Similarly, Oceania suffered minimal impact, in part due to its proximity to Asian markets.

Terminology

Two definitions of the term "economic recession" exist: one sense referring generally to "a period of reduced economic activity" and ongoing hardship; and a technical definition used in economics, which is defined operationally, specifically the contraction phase of a business cycle with two or more consecutive quarters of GDP contraction (negative GDP growth rate). The latter is typically used to influence abrupt changes in monetary policy.

Under the technical definition, the recession ended in the United States in June or July 2009.

Journalist Robert Kuttner has argued that 'The Great Recession' is a misnomer. According to Kuttner, "recessions are mild dips in the business cycle that are either self-correcting or soon cured by modest fiscal or monetary stimulus. Because of the continuing deflationary trap, it would be more accurate to call this decade's stagnant economy The Lesser Depression or The Great Deflation."

Overview

The Great Recession met the IMF criteria for being a global recession only in the single calendar year 2009. That IMF definition requires a decline in annual real world GDP per capita. Despite the fact that quarterly data are being used as recession definition criteria by all G20 members, representing 85% of the world GDP, the International Monetary Fund (IMF) has decided – in the absence of a complete data set – not to declare/measure global recessions according to quarterly GDP data. The seasonally adjusted PPP‑weighted real GDP for the G20‑zone, however, is a good indicator for the world GDP, and it was measured to have suffered a direct quarter on quarter decline during the three quarters from Q3‑2008 until Q1‑2009, which more accurately mark when the recession took place at the global level.

According to the U.S. National Bureau of Economic Research (the official arbiter of U.S. recessions), the recession began in December 2007 and ended in June 2009, and thus extended over eighteen months.

The years leading up to the crisis were characterized by an exorbitant rise in asset prices and associated boom in economic demand. Further, the U.S. shadow banking system (i.e., non-depository financial institutions such as investment banks) had grown to rival the depository system yet was not subject to the same regulatory oversight, making it vulnerable to a bank run.

U.S. mortgage-backed securities, which had risks that were hard to assess, were marketed around the world, as they offered higher yields than U.S. government bonds. Many of these securities were backed by subprime mortgages, which collapsed in value when the U.S. housing bubble burst during 2006 and homeowners began to default on their mortgage payments in large numbers starting in 2007.

The emergence of subprime loan losses in 2007 began the crisis and exposed other risky loans and over-inflated asset prices. With loan losses mounting and the fall of Lehman Brothers on September 15, 2008, a major panic broke out on the inter-bank loan market. There was the equivalent of a bank run on the shadow banking system, resulting in many large and well established investment banks and commercial banks in the United States and Europe suffering huge losses and even facing bankruptcy, resulting in massive public financial assistance (government bailouts).

The global recession that followed resulted in a sharp drop in international trade, rising unemployment and slumping commodity prices. Several economists predicted that recovery might not appear until 2011 and that the recession would be the worst since the Great Depression of the 1930s. Economist Paul Krugman once commented on this as seemingly the beginning of "a second Great Depression".

Governments and central banks responded with fiscal policy and monetary policy initiatives to stimulate national economies and reduce financial system risks. The recession renewed interest in Keynesian economic ideas on how to combat recessionary conditions. Economists advise that the stimulus measures such as quantitative easing (pumping money into the system) and holding down central bank wholesale lending interest rates should be withdrawn as soon as economies recover enough to "chart a path to sustainable growth".

The distribution of household incomes in the United States became more unequal during the post-2008 economic recovery. Income inequality in the United States grew from 2005 to 2012 in more than two thirds of metropolitan areas. Median household wealth fell 35% in the U.S., from $106,591 to $68,839 between 2005 and 2011.

Causes

Panel reports

The U.S. Financial Crisis Inquiry Commission, composed of six Democratic and four Republican appointees, reported its majority findings in January 2011. It concluded that "the crisis was avoidable and was caused by:

Widespread failures in financial regulation, including the Federal Reserve's failure to stem the tide of toxic mortgages;

Dramatic breakdowns in corporate governance including too many financial firms acting recklessly and taking on too much risk;

An explosive mix of excessive borrowing and risk by households and Wall Street that put the financial system on a collision course with crisis;

Key policy makers ill prepared for the crisis, lacking a full understanding of the financial system they oversaw; and systemic breaches in accountability and ethics at all levels."

There were two Republican dissenting FCIC reports. One of them, signed by three Republican appointees, concluded that there were multiple causes. In his separate dissent to the majority and minority opinions of the FCIC, Commissioner Peter J. Wallison of the American Enterprise Institute (AEI) primarily blamed U.S. housing policy, including the actions of Fannie and Freddie, for the crisis. He wrote: "When the bubble began to deflate in mid-2007, the low quality and high risk loans engendered by government policies failed in unprecedented numbers."

In its "Declaration of the Summit on Financial Markets and the World Economy," dated November 15, 2008, leaders of the Group of 20 cited the following causes:

During a period of strong global growth, growing capital flows, and prolonged stability earlier this decade, market participants sought higher yields without an adequate appreciation of the risks and failed to exercise proper due diligence. At the same time, weak underwriting standards, unsound risk management practices, increasingly complex and opaque financial products, and consequent excessive leverage combined to create vulnerabilities in the system. Policy-makers, regulators and supervisors, in some advanced countries, did not adequately appreciate and address the risks building up in financial markets, keep pace with financial innovation, or take into account the systemic ramifications of domestic regulatory actions.

Federal Reserve Chair Ben Bernanke testified in September 2010 before the FCIC regarding the causes of the crisis. He wrote that there were shocks or triggers (i.e., particular events that touched off the crisis) and vulnerabilities (i.e., structural weaknesses in the financial system, regulation and supervision) that amplified the shocks. Examples of triggers included: losses on subprime mortgage securities that began in 2007 and a run on the shadow banking system that began in the middle of 2007, which adversely affected the functioning of money markets. Examples of vulnerabilities in the private sector included: financial institution dependence on unstable sources of short-term funding such as repurchase agreements or Repos; deficiencies in corporate risk management; excessive use of leverage (borrowing to invest); and inappropriate usage of derivatives as a tool for taking excessive risks. Examples of vulnerabilities in the public sector included: statutory gaps and conflicts between regulators; ineffective use of regulatory authority; and ineffective crisis management capabilities. Bernanke also discussed "Too big to fail" institutions, monetary policy, and trade deficits.

Narratives

There are several "narratives" attempting to place the causes of the recession into context, with overlapping elements. Five such narratives include:

There was the equivalent of a bank run on the shadow banking system, which includes investment banks and other non-depository financial entities. This system had grown to rival the depository system in scale yet was not subject to the same regulatory safeguards. Its failure disrupted the flow of credit to consumers and corporations.

The U.S. economy was being driven by a housing bubble. When it burst, private residential investment (i.e., housing construction) fell by over four percent of GDP. Consumption enabled by bubble-generated housing wealth also slowed. This created a gap in annual demand (GDP) of nearly $1 trillion. The U.S. government was unwilling to make up for this private sector shortfall.

Record levels of household debt accumulated in the decades preceding the crisis resulted in a balance sheet recession (similar to debt deflation) once housing prices began falling in 2006. Consumers began paying off debt, which reduces their consumption, slowing down the economy for an extended period while debt levels are reduced.

U.S. government policies encouraged home ownership even for those who could not afford it, contributing to lax lending standards, unsustainable housing price increases, and indebtedness.

Wealthy and middle-class house flippers with mid-to-good credit scores created a speculative bubble in house prices, and then wrecked local housing markets and financial institutions after they defaulted on their debt en masse.

Underlying narratives #1–3 is a hypothesis that growing income inequality and wage stagnation encouraged families to increase their household debt to maintain their desired living standard, fueling the bubble. Further, this greater share of income flowing to the top increased the political power of business interests, who used that power to deregulate or limit regulation of the shadow banking system.

Narrative #5 challenges the popular claim (narrative #4) that subprime borrowers with shoddy credit caused the crisis by buying homes they couldn't afford. This narrative is supported by new research showing that the biggest growth of mortgage debt during the U.S. housing boom came from those with good credit scores in the middle and top of the credit score distribution – and that these borrowers accounted for a disproportionate share of defaults.

Trade imbalances and debt bubbles

The Economist wrote in July 2012 that the inflow of investment dollars required to fund the U.S. trade deficit was a major cause of the housing bubble and financial crisis: "The trade deficit, less than 1% of GDP in the early 1990s, hit 6% in 2006. That deficit was financed by inflows of foreign savings, in particular from East Asia and the Middle East. Much of that money went into dodgy mortgages to buy overvalued houses, and the financial crisis was the result."

In May 2008, NPR explained in their Peabody Award winning program "The Giant Pool of Money" that a vast inflow of savings from developing nations flowed into the mortgage market, driving the U.S. housing bubble. This pool of fixed income savings increased from around $35 trillion in 2000 to about $70 trillion by 2008. NPR explained this money came from various sources, "[b]ut the main headline is that all sorts of poor countries became kind of rich, making things like TVs and selling us oil. China, India, Abu Dhabi, Saudi Arabia made a lot of money and banked it."

Describing the crisis in Europe, Paul Krugman wrote in February 2012 that: "What we're basically looking at, then, is a balance of payments problem, in which capital flooded south after the creation of the euro, leading to overvaluation in southern Europe."

Monetary policy

Another narrative about the origin has been focused on the respective parts played by public monetary policy (notably in the US) and by the practices of private financial institutions. In the U.S., mortgage funding was unusually decentralised, opaque, and competitive, and it is believed that competition between lenders for revenue and market share contributed to declining underwriting standards and risky lending.

While Alan Greenspan's role as Chairman of the Federal Reserve has been widely discussed, the main point of controversy remains the lowering of the Federal funds rate to 1% for more than a year, which, according to Austrian theorists, injected huge amounts of "easy" credit-based money into the financial system and created an unsustainable economic boom. There is an argument that Greenspan's actions in the years 2002–2004 were actually motivated by the need to take the U.S. economy out of the early 2000s recession caused by the bursting of the dot-com bubble: although by doing so he did not avert the crisis, but only postponed it.

High private debt levels

Another narrative focuses on high levels of private debt in the US economy. USA household debt as a percentage of annual disposable personal income was 127% at the end of 2007, versus 77% in 1990. Faced with increasing mortgage payments as their adjustable rate mortgage payments increased, households began to default in record numbers, rendering mortgage-backed securities worthless. High private debt levels also impact growth by making recessions deeper and the following recovery weaker. Robert Reich claims the amount of debt in the US economy can be traced to economic inequality, assuming that middle-class wages remained stagnant while wealth concentrated at the top, and households "pull equity from their homes and overload on debt to maintain living standards".

The IMF reported in April 2012: "Household debt soared in the years leading up to the downturn. In advanced economies, during the five years preceding 2007, the ratio of household debt to income rose by an average of 39 percentage points, to 138 percent. In Denmark, Iceland, Ireland, the Netherlands, and Norway, debt peaked at more than 200 percent of household income. A surge in household debt to historic highs also occurred in emerging economies such as Estonia, Hungary, Latvia, and Lithuania. The concurrent boom in both house prices and the stock market meant that household debt relative to assets held broadly stable, which masked households' growing exposure to a sharp fall in asset prices. When house prices declined, leading to the 2008 financial crisis, many households saw their wealth shrink relative to their debt, and, with less income and more unemployment, found it harder to meet mortgage payments. By the end of 2011, real house prices had fallen from their peak by about 41% in Ireland, 29% in Iceland, 23% in Spain and the United States, and 21% in Denmark. Household defaults, underwater mortgages (where the loan balance exceeds the house value), foreclosures, and fire sales are now endemic to a number of economies. Household deleveraging by paying off debts or defaulting on them has begun in some countries. It has been most pronounced in the United States, where about two-thirds of the debt reduction reflects defaults."

Pre-recession warnings

The onset of the economic crisis took most people by surprise. A 2009 paper identifies twelve economists and commentators who, between 2000 and 2006, predicted a recession based on the collapse of the then-booming housing market in the United States: Dean Baker, Wynne Godley, Fred Harrison, Michael Hudson, Eric Janszen, Med Jones Steve Keen, Jakob Brøchner Madsen, Jens Kjaer Sørensen, Kurt Richebächer, Nouriel Roubini, Peter Schiff, and Robert Shiller.

Housing bubbles

By 2007, real estate bubbles were still under way in many parts of the world, especially in the United States, France, the United Kingdom, Spain, the Netherlands, Australia, the United Arab Emirates, New Zealand, Ireland, Poland, South Africa, Greece, Bulgaria, Croatia, Norway, Singapore, South Korea, Sweden, Finland, Argentina, the Baltic states, India, Romania, Ukraine and China. U.S. Federal Reserve Chairman Alan Greenspan said in mid-2005 that "at a minimum, there's a little 'froth' [in the U.S. housing market]...it's hard not to see that there are a lot of local bubbles".

The Economist, writing at the same time, went further, saying, "[T]he worldwide rise in house prices is the biggest bubble in history". Real estate bubbles are (by definition of the word "bubble") followed by a price decrease (also known as a housing price crash) that can result in many owners holding negative equity (a mortgage debt higher than the current value of the property).

Ineffective regulation

Derivatives

Several sources have noted the failure of the US government to supervise or even require transparency of the financial instruments known as derivatives. Derivatives such as credit default swaps (CDSs) were unregulated or barely regulated. Michael Lewis noted CDSs enabled speculators to stack bets on the same mortgage securities. This is analogous to allowing many persons to buy insurance on the same house. Speculators that bought CDS protection were betting significant mortgage security defaults would occur, while the sellers (such as AIG) bet they would not. An unlimited amount could be wagered on the same housing-related securities, provided buyers and sellers of the CDS could be found. When massive defaults occurred on underlying mortgage securities, companies like AIG that were selling CDS were unable to perform their side of the obligation and defaulted; U.S. taxpayers paid over $100 billion to global financial institutions to honor AIG obligations, generating considerable outrage.

A 2008 investigative article in The Washington Post found leading government officials at the time (Federal Reserve Board Chairman Alan Greenspan, Treasury Secretary Robert Rubin, and SEC Chairman Arthur Levitt) vehemently opposed any regulation of derivatives. In 1998, Brooksley E. Born, head of the Commodity Futures Trading Commission, put forth a policy paper asking for feedback from regulators, lobbyists, and legislators on the question of whether derivatives should be reported, sold through a central facility, or whether capital requirements should be required of their buyers. Greenspan, Rubin, and Levitt pressured her to withdraw the paper and Greenspan persuaded Congress to pass a resolution preventing CFTC from regulating derivatives for another six months – when Born's term of office would expire. Ultimately, it was the collapse of a specific kind of derivative, the mortgage-backed security, that triggered the economic crisis of 2008.

Shadow banking system

Paul Krugman wrote in 2009 that the run on the shadow banking system was the fundamental cause of the crisis. "As the shadow banking system expanded to rival or even surpass conventional banking in importance, politicians and government officials should have realised that they were re-creating the kind of financial vulnerability that made the Great Depression possible – and they should have responded by extending regulations and the financial safety net to cover these new institutions. Influential figures should have proclaimed a simple rule: anything that does what a bank does, anything that has to be rescued in crises the way banks are, should be regulated like a bank." He referred to this lack of controls as "malign neglect".

During 2008, three of the largest U.S. investment banks either went bankrupt (Lehman Brothers) or were sold at fire sale prices to other banks (Bear Stearns and Merrill Lynch). The investment banks were not subject to the more stringent regulations applied to depository banks. These failures exacerbated the instability in the global financial system. The remaining two investment banks, Morgan Stanley and Goldman Sachs, potentially facing failure, opted to become commercial banks, thereby subjecting themselves to more stringent regulation but receiving access to credit via the Federal Reserve. Further, American International Group (AIG) had insured mortgage-backed and other securities but was not required to maintain sufficient reserves to pay its obligations when debtors defaulted on these securities. AIG was contractually required to post additional collateral with many creditors and counter-parties, touching off controversy when over $100 billion of U.S. taxpayer money was paid out to major global financial institutions on behalf of AIG. While this money was legally owed to the banks by AIG (under agreements made via credit default swaps purchased from AIG by the institutions), a number of Congressmen and media members expressed outrage that taxpayer money was used to bail out banks.

Economist Gary Gorton wrote in May 2009